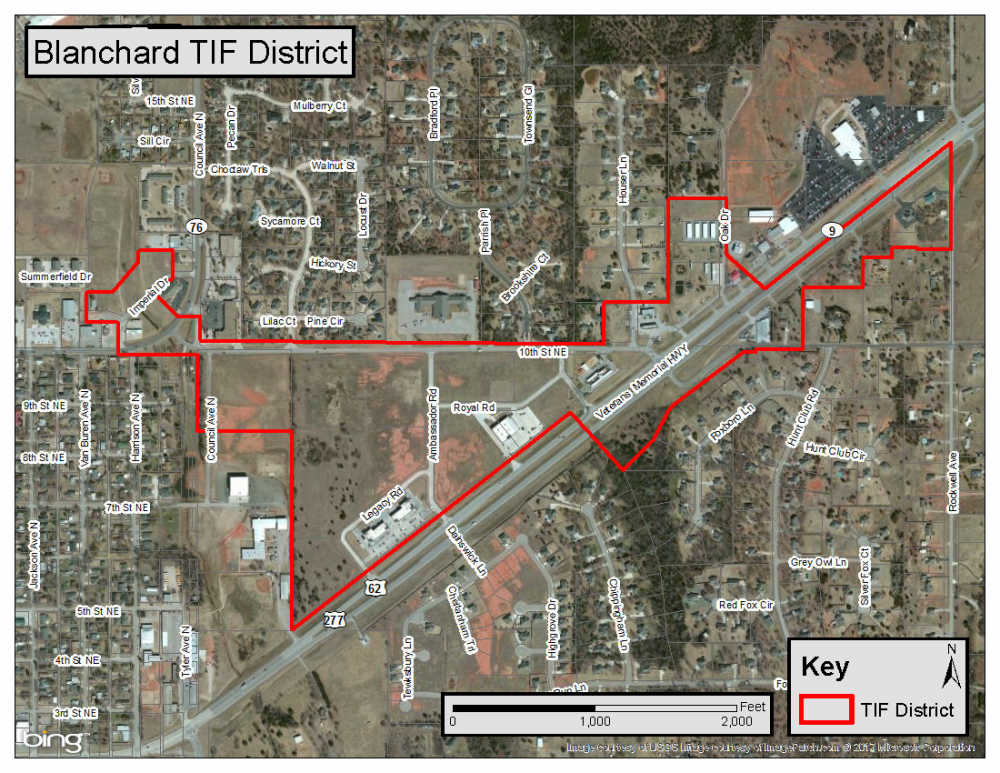

Blanchard TIF District No. 1

Introduction

- What is Tax Increment Financing?

Tax Increment Financing (TIF) is an economic development tool authorized by the Oklahoma Constitution and state statute to permit cities, towns, and counties to use local taxes and fees to finance certain public costs of development and redevelopment. Projects financed with TIF must serve a public purpose such as redeveloping blighted areas, providing employment opportunities and improving the tax base.

- How does TIF work?

When a TIF district is established, the assessed value of all taxable property within the district (or, in the case of a sales tax increment district, the sales tax revenue from within the district) is established as a base. For the district’s duration – until the project costs are paid, not to exceed twenty-five (25) years – any growth of tax revenues above the base are available to the city, town, or county to finance public project costs. Taxes generated from base assessed value (or an amount equal to the base sales tax) continue to be paid to the various taxing jurisdictions (county, school district, vo-tech district, library system, health department.)

- Why a TIF?

For a city, town, or county to use TIF to help finance a development or redevelopment project, it must determine that, among other things, investment, development and economic growth are difficult but possible if TIF is utilized. It must also determine that TIF is not being proposed for an area where investment, development, and economic growth would have occurred anyway and that TIF is being used to supplement and not supplant or replace normal public functions and services. Projects that meet these conditions should have no negative impact on the affected taxing jurisdictions, since they use only tax revenues that, without the use of TIF, would not have been generated.

- What about public input?

The governing body of the city, town, or county considering a TIF project must appoint a review committee made up of representatives of the affected taxing jurisdictions, the planning commission with jurisdiction over the project area, the city, town, or county considering the project (whose representative serves as chairperson), and the public at large. The review committee then must make determinations as to the eligibility of the project and the financial impact, if any, of the project on the taxing jurisdictions, as well as a recommendation to the governing body whether to approve the project.The Blanchard Planning Commission must separately consider the proposed project and determine whether it conforms to the comprehensive (master) plan for the area. All meetings of the review committee, planning commission and city council are subject to open meeting laws.

Prior to adoption of a TIF project, the city council must hold two public meetings. The first is solely to provide the public information about the proposed project with the Planning Commission; and the second is a public hearing to provide an opportunity for the public to be heard in favor of or opposition to the proposed project.

If the city council votes to approve the proposed project contrary to the recommendation of the review committee, it must do so by a two-thirds majority. Any change to the area to be included, any substantial change in the proposed project, or any amendment of an approved plan affecting more than five (5%) percent of the district’s area or five (5%) percent of the project costs must be reviewed and approved by the review committee, planning commission, and city council in the same manner as the original proposal.

- How may TIF be used?

Oklahoma’s Local Development Act governs TIF uses. Tax increment revenues must be spent for approved public costs of development and redevelopment within geographic areas referred to as project areas.

- TIF uses include:

- Capital costs, including costs of repair or reconstruction of public works and public improvements

- Financing costs, including costs associated with the issuance of bonds, if used

- Real property purchase

- Environmental remediation associated with public projects

- Professional services costs

- Direct administrative costs

- Financing methods:

- Pay-As-You-Go: The City pays for TIF-eligible costs, and is reimbursed from the increment of increased tax revenue generated by the development (the "Increment").

- Bonds: Bonds are issued "up front" to pay for public improvements (capital costs) and are repaid with the Increment.

- What are some of the benefits of TIF?

TIF allows cities, towns and counties to simulate revitalization activities that the private sector is unwilling or unable to undertake. By using TIF, cities, towns, and counties have tools to:- Leverage economic revitalization;

- Supplement other public functions, services, efforts and programs, including Oklahoma Main Street Program, Oklahoma Enterprise Zone Act, historic preservation, and other locally implemented economic development efforts;

- Enhance conservation, preservation, and rehabilitation efforts;

- Encourage residential development;

- Enhance neighborhood stability;

- Remediate environmental damage;

- Enhance the residential and/or commercial tax base;

- Create and retain jobs.

- Create and retain jobs.

By setting a base assessed value of property in redevelopment areas, cities, towns and counties in effect buffer affected taxing jurisdictions from deterioration of the local tax base.